Viewpoints

INVESTOR INTELLIGENCE

S&P 500:

The S&P 500 finished the week 2% lower, at 3852.36. This brings the index down nearly 20% for this year, potentially the worst yearly performance since the financial crisis of 2008. During the past week, the energy sector held up the best, while consumer cyclicals, materials, communication & technology performed the weakest. At the end of last week slightly more than half the 500 stocks in the index were trading above their 50 day averages.

Last week’s report noted the potential for triggering stop losses upon declining more than 5% below the high of recent weeks. If the selling trend continues, the index could soon be retesting the previous lows of October around 3491. There also remains the potential for a sell-off into the end of the year, similar to what occurred in 2018 during the last round of quantitative tightening by the Fed.

Chart: the 13 day average crossing under the 26 day average for the 5th time this year.

NOTEWORTHY:

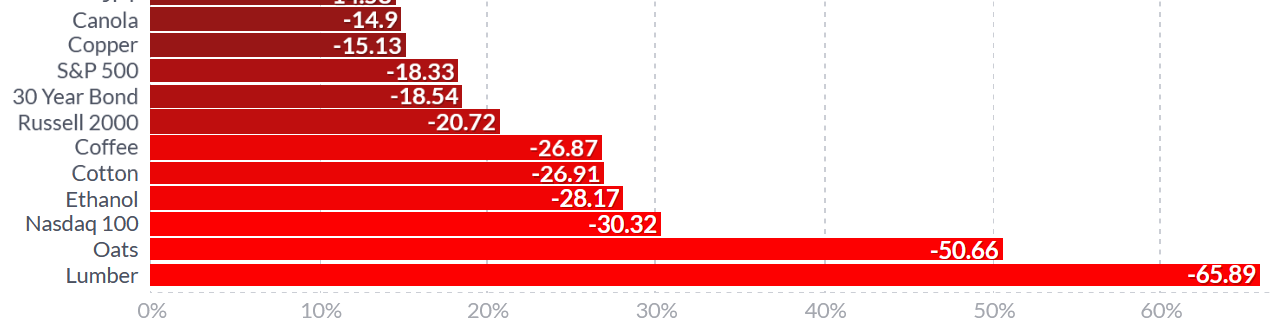

With most commodities being down anywhere from 12% to 65% this year, when do we talk about deflation?

With prices for raw commodities collapsing like this, how hard will it be for the Fed to get inflation down to its target near 2%? Right now the market inflation expectations 5 years out sits just slightly above 2% on the 5y forward and 5y breakeven inflation rates.

WATCHLIST:

Some of the names we’re keeping our eyes on this week :

TSLA

Tesla is still among the top 10 largest market cap companies of the S&P500 despite being down by almost 63% this year. Tesla just had its largest weekly decline since the 2020 financial crisis. The 3rd largest shareholder KoGuan Leo has been calling for Elon Musk to step down from CEO.

NKE

This Dow 30 index component reports after the close Tuesday , 20th. Forward earnings multiple at 34x seem high considering the outlook for earnings decline of -30% this fiscal year. Investors will be watching for improvement with the growing inventory problem. The supply-chain problems in recent years led to increased ordering of products. Last Q they reported nearly $10B in bloated inventory, a 44.23% increase year-over-year.

FDX

FedEx reports after the close Tuesday , 20th. The stock has lost about a third of market value so far this year but remains a favorite amongst institutional investors who own 74% of the shares. Dow theory suggests that the transports ‘lead the way’ in that the transportation sector gives a strong indication of the broader economic trend. Because transportation stocks are sensitive to changes in economic activity, the latest report from FedEx may give investors some further insight into the current demand for shipping and the broader economy as a whole.

MU

Micron reports fiscal Q1 after the close Wednesday, 21st. The memory and storage chip company has lost nearly half its market value this year and is struggling to deal with a buildup of excess inventory and reduced demand. At the lows of the year, the stock was trading just slightly above book value. Last month the company announced plans to reduce production and capex spending cuts but still plans to invest over $150 billion over the next decade on memory chip manufacturing and R&D.